This week will probably be one of many busiest of the 12 months, crammed with earnings studies, a Federal Reserve assembly, substantial financial knowledge, and a Treasury Quarterly Refunding announcement.

Though there are blended opinions concerning the affect of the Quarterly Refunding Announcement, it’s prone to find yourself as a non-event. Particulars will begin to floor on Monday afternoon, with the official bulletins set for Wednesday morning.

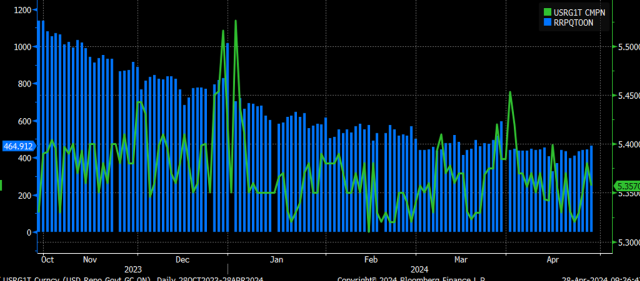

There’s some hypothesis on social media that the Treasury Common Account (TGA) will probably be considerably diminished, probably releasing a wave of liquidity into the markets.

Whereas a discount from the present $900 billion to about $750 billion is feasible, it’s unbelievable that it’ll lower to $100 billion.

If the Treasury reduces invoice issuance, a number of the funds which have moved out of the reverse repo facility in current months may begin to circulate again. If there’s an extra of money within the in a single day funding markets, in a single day charges might drop to the reverse repo price of 5.3%.

If charges fall too low, the cash will seemingly discover its means again into the Reverse Repo Program (RRP), which might assist drain liquidity from the system, particularly if the reverse repo facility will increase sooner than the TGA decreases.

For the reason that finish of March, the in a single day price has usually been trending decrease, and the money within the repo facility has been usually trending larger. So, the small print we get within the subsequent few days might be essential, particularly if invoice issuance is internet destructive.

This week’s Federal Reserve assembly might be extra vital for credit score spreads than anything. Monetary circumstances eased considerably when the Fed pivoted and indicated potential price cuts in December.

That course of started in November when Powell prompt that price hikes had been practically over. Will this assembly function the catalyst to start out tightening these circumstances once more if Powell means that the variety of price cuts anticipated in March is likely to be diminished, with the June assembly presumably taking all of them away? It’s a risk.

To date, the bottom level for spreads was proper across the March FOMC assembly.

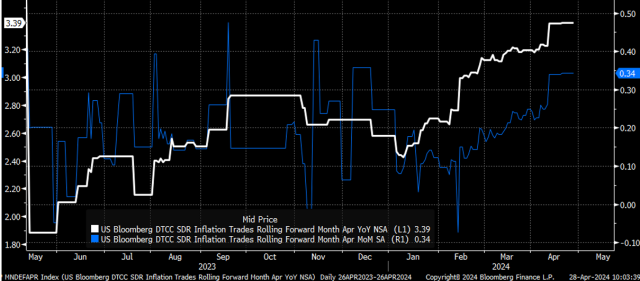

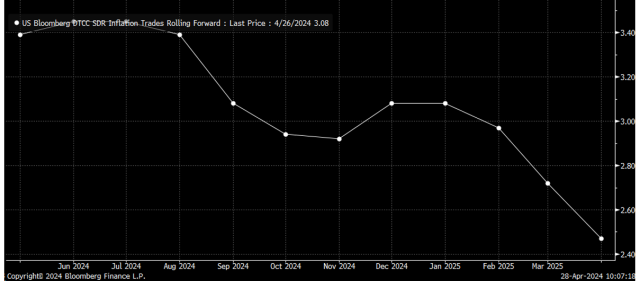

One purpose the Fed could remove all price cuts by June is that the April CPI swaps are anticipated to indicate a rise of 0.34% month-over-month and by 3.4% year-over-year. Let’s face it: 0.34% is simply 0.01% away from 0.35%, which then rounds as much as 0.4%. If the CPI studies one other 0.4% in April for the third consecutive month, it is not going to bode nicely for the speed minimize outlook.

Primarily based on the present CPI pricing, it will likely be difficult to see charges beneath 3.0% till February 2025. So, if the Fed is hoping for a sequence of favorable studies earlier than beginning to minimize charges, they could have to attend till Might 2025—a minimum of if the present development continues and swap pricing is correct.

This means that the 2-year Treasury charges will proceed to rise and push by means of the bull flag.

US 2-Yr Yield-Day by day Chart

The 10-year can also be prone to climb larger and attain round 5% after breaking above resistance at 4.65% on the finish of final week.

That is in all probability why the greenback also needs to proceed to strengthen, push larger, and get away of its bull flag.

In the meantime, the S&P 500 rose this week to achieve the 20-day transferring common, could be very near the 50-day transferring common, and is approaching the downtrend line. So, this week will probably be pivotal in figuring out whether or not the downtrend within the SPX ought to persist.